Distressed Property Sales on the Rise Post-Pandemic

As the last few states move toward the process of a multi-phased re-opening, and business resumes, we are beginning to get a grasp on what the future commercial real estate market will look like. Up until the Coronavirus hit, the real estate market was one of the strongest we have seen. But, as predicted by CoStar, the world leader in commercial real estate information database, distressed properties will be the product in demand in the coming months. As of now, distressed sale properties are few and far between as people are holding on to what they have not wanting to realize that property values have declined.

As reported by Costar, The Federal Reserve recently released its latest semiannual stability report that projected commercial real estate may undergo a “substantial repricing.” The Fed declined to say how much of a repricing but noted property values were already elevated, which increases the risk of steep declines.

According to costar.com, “Current sales volumes are smaller compared to February before the pandemic wreaked havoc on capital markets. The $15.1 billion in sales reported in April was down about 70% from February’s volume of $55.9 billion, according to CoStar data. That trend is continuing this month. The properties trading now are generally the better quality, cash-flowing ones. That phenomenon is evident in sales pricing per square foot or per unit. Industrial properties are getting sold at per-square-foot prices 22.5% more than year-end 2019 rates. Office properties going at prices 26.3% higher; multifamily, 3% higher. Only retail property prices are down from the pre-COVID-19 prices, down 14.2%.”

People are looking for stability at a time like this, so deals that cash-flow will continue to be very attractive. On the flip side of that coin, now is a great time to take advantage of depressed pricing and distressed sales could be on the rise. CoStar estimates that there could be $146 billion in distressed sales in 2021 and 2022. It is possible that projections could even exceed what we saw happen in 2008 with the Great Recession when CoStar recorded $176 billion of distressed sales over an eight year period.

“Historical CoStar data shows that when distressed sales flood the market in a short time period, properties are liquidated at prices not only much lower than their outstanding loan balance, but also much lower than the market value of similar properties in the same location. Properties could sell at an average of one-third of their pre-coronavirus value, according to a CoStar analysis, which is similar in severity to the Great Recession,” according to CoStar.com.

Who knows exactly what the future markets will look like after an unprecedented event such as COVID-19, but looking to the past, distressed properties seem to be a safe bet as the market beings it’s climb back up to the top where it was pre-pandamic.

Sources: costar.com [Article] https://www.costar.com/article/147645783/distressed-sales-from-pandemic-could-exceed-volume-of-great-recession

Demand for Industrial Space

Historically, industrial real estate has been a popular asset. It is relativity stable, can stand the test of time, has favorable occupancy, a steady demand, longer term tenants, lower maintenance, and lower re-tenanting costs. It has proven this even more so during the current pandemic, with many of the crucial services that were essential pointing us in the direction and showing us the need for even more industrial space.

Since March many states have issued stay-at-home orders which has more people then ever turning to online shopping and convinces such as grocery pickup or delivery services to be able to get what they need while sheltering in place. While e-commerce was already gaining popularity and taking away from brick and mortar stores, the pandemic has shifted this into over drive and will affect the way we operate going forward.

During this pandemic, supply chain operations and industrial warehouses have been the glue that has kept our economy going. It has also shown us that our current system is not strong enough to support a spike in demand. As the need grows for industrial space, business are re-thinking where they are purchasing space and looking for more local locations in order order to enhance their delivery speeds. “Smaller, last-mile industrial facilities are positioned throughout metro areas at a higher volume, allowing retailers to be nimbler in their delivery model and efficiently complete the “last mile” to consumer residences. The progression to last-mile industrial facilities provides insight into where the market has evolved and translates to a significant development opportunity.” according to nreionline.com.

This demand for virtual business is also showing a rise in demand for temperature controlled spaces to accommodate for grocery delivery.

“When examining e-commerce’s delivery logistics throughout the past decade, the average industrial tenant size has decreased, and tenants moved to infill locations as major retailers have shifted their logistics footprints to meet online sales growth. At the beginning of this real estate cycle, retail giants built large distribution centers—often around 1 million sq. ft.— positioned strategically throughout the nation. In recent years, a new wave of the logistics network has unfolded as these retailers started seeking shallow bay, urban and centrally located industrial facilities in order to enhance their delivery speeds.” as stated by nreionline.com.

As markets continue to open, the need for industrial space is remaining constant. The physical space is still needed to stage product, and pack trucks can not be replicated digitally and will more then likely stay the same.

According to a recent article from nreionline.com, “(Bloomberg)—Prologis Inc., the largest owner of warehouses in the U.S., is getting a boost as social- distancing pushes consumers deeper into the embrace of e-commerce.

Companies including Amazon.com Inc. and Walmart Inc. have an “almost insatiable” appetite for more warehouse space, Chief Executive Officer Hamid Moghadam said in an interview on Tuesday. “We’re not seeing those guys slow down, they continue to be very active in making new deals,” Moghadam said. “The strong continue to be taking a lot of space.”

Although nothing is ever a sure bet, as it stands now, industrial real estate is still the stable and consistent asset it has always been. It may even serve as a path forward as we begin to dig out way out of the current situation and lay the ground work for what the future will look like.

Source

nreionline.com [Article] https://www.nreionline.com/industrial/industrial-development-offers-attractive-opportunity-path-forward

nreionline.com [Article] https://www.nreionline.com/industrial/warehouse-giant-seeing-insatiable-demand-amazon-walmart

How Stimulus Helped Boost May Job Growth

Road to Recovery Under Optimistic Conditions

Weighing Your Financial Options...Is a Workout Right for You?

The United States is closing on it’s third month since the news hit of the COVID-19 outbreak and all of the economic uncertainty and financial strain that comes along with effectively shutting down the world’s top economy. As access to capital continues to tighten, and government assistance is difficult to come by, the problems are compounding. During times like this companies are looking for more non-traditional ways of raising funds to help them navigate day to day operations until the pendulum starts to move in the other direction.

A workout is one avenue to consider. It is an excellent tool for companies that are in distress, but have the vision and planning to see that with a capital investment they can begin to move away from the red and toward the green in a set amount of time. A workout combines a well laid out plan based on documentation, financial planning and an injection of capital. Businesses who are good candidates for this option are ones who can prove a detailed plan to a lender of how the monetary investment will allow them to move forward and become cash positive again.

According to CCIM.com, a successful workout depends on two equally critical elements: the property must be capable of being turned around, stabilized, and profitably sold or refinanced; and the borrower must have the right background, reputation, commitment, and experience to obtain the financing and see the project through to completion.

Several factors must be present for a project to be worked out.

The debt must reflect a sensible and realistic loan-to-value ratio based on current economic conditions. Undertaking a workout that is over leveraged as compared to market value is a waste of time and money.

The turnaround plan must be based on conservative real estate fundamentals. Leasing, sale, expense, and cost targets must be obtainable.

The project's plan must reflect current economic conditions. For example, an owner shouldn't expect to turn his warehouse into a telcom hotel in today's economic climate.

The exit strategy, or repayment plan, has to be based on controllable results. Relying on a refinancing in three years based on regular rental increases, stable occupancies, and today's low interest rates would be a mistake.

Even with the best projects, workouts only are possible with the right borrower. Borrowers should have experience in the particular property type; commitment to the project, shown by an infusion of fresh equity; and a good reputation. Workout lenders will investigate a borrower's background to see how he has handled himself in similar situations. They will want to know if former lenders view the borrower favorably.

Once you have determined that a workout is right for you and you have the proper plan in place, the next step is to look around and see where to go for financing. Since financing a workout is typically a complicated situation going to a one-stop-shop is the easiest path to take.

Per CCIM.com, there are three major benefits to using a single source to financing your workout. First, it requires only one round of due diligence, saving valuable time and money. Second, fewer attorneys are involved, thereby speeding up the transaction. Third, the need for inter- creditor negotiations and documentation is eliminated, often making this the preferred structure for borrowers. Last, less equity must be raised and less, if any, ownership is relinquished.

The third and final piece to this puzzle is to locate a lender. The easiest way to locate a workout lender is to find an institution that has aggressive mezzanine and equity programs such as opportunity funds, Wall Street subsidiaries, institutional lenders, hedge funds and private lenders. These types of lenders will typically see these higher risk situations as an opportunity for better than average returns. All in all, in the right circumstances, with the correct plan, a workout can be a win win for all parties involved.

Source:https://www.ccim.com/cire-magazine/articles/struggling-properties-can-exercise-workout-options-improve-financial-health/

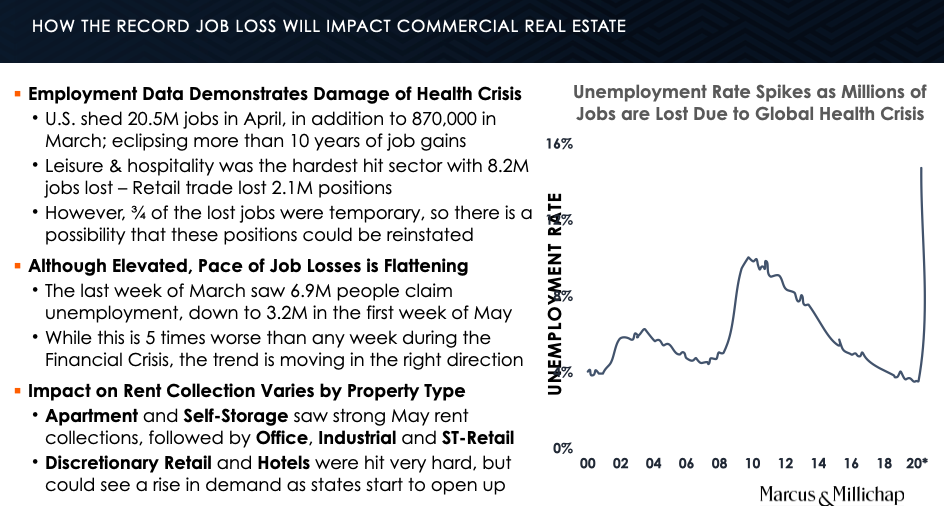

How Record Job Losses Impact Real Estate

TO WATCH THE FULL VIDEO, CLICK HERE.

How Businesses and Tenants are Finding Creative Ways to Pay the Bills

As millions of people are told to stay home from work and shelter in their homes the question remains, if people are not going to work and making money how can they afford to stay in their homes? How can business keep the doors open if they are not bringing in money to pay the rent? This may be the biggest catch-22 the United States has been presented with since the Great Recession in 2007-2009.

According to data collected from ccim.com, here are a few ways landlords and tenants are dealing with these tumultuous circumstances.

Rent Reduction: The landlord can reduce the tenant's rent for a portion or all of the term left on the lease. The usual forms of rent reduction are to reduce the base rent, operating expenses, or both. In regard to retail, it is possible to convert base rent to percentage rent.

Rent Deferral: In this case, the landlord can defer a portion of the tenant's rent but would require them to repay the rent deferred at a later time, either in a lump sum or by increasing subsequent payments. A variation of rent deferral could be to cap or set a base year to operating expenses for a short or extended period of time.

Rent Abatement: If a tenant is significantly past due on rent payments, a landlord may agree to forgive a certain amount of the past due rent if the tenant remains current thereafter.

Loan Conversion: Rather than abating past due rent, a landlord may agree to convert the past due rent into a loan payable over time. The tenant would, however, continue to pay the current rent. The loan is then evidenced by a promissory note that is cross-defaulted with the lease.

Application of Deposit: If the landlord holds a deposit, this amount could be credited against the tenant's current obligations.

Subletting: Bringing in a new tenant (for part of or all of the rented space) could reduce or eliminate the rent obligations while replacing revenue for the landlord.

Unfortunately, this problem extends to other markets beyond that of Americans and their homes. This issue is having a serve impact on business and their ability to pay rent during a time when most have been told to shut their doors to help perpetuate social distancing.

According to The Certified Commercial Investment Institute website (ccim.com), here are their predictions as to the effects COVID-19 will have on the retail, hospitality, Office, Industrial and Multifamily markets.

Retail: Retail will see a bifurcated reaction to this economic downturn. Storefronts selling consumer staples - like Walmart, CVS, and grocery stores-will thrive, while dine-in restaurants, for example, could remain closed for the foreseeable future.

Hospitality: Unsurprisingly, hospitality has been decimated by the national response to the pandemic. CCIM Institute Chief Economist K.C. Conway recommends those in the sector ask themselves some basic questions. “For those that own hospitality assets and invest in that space, you need to step back and reflect on what brought you to that property type. Why? Where were you going into this particular period? The market had near record revenues per available room, average daily occupancy, and rental rates. … Whether I'm a hospitality REIT, hotel owner, or I've got properties, I want to negotiate with my lenders for some debt restructuring.”

Office: The office leasing market is likely to suffer in the short-term due to COVID-19 as layoffs diminish tenants' overall need for space and, in many cases, set aside expansion plans they may have had. In addition, tenants who remain in the market for additional space will have a difficult time touring properties. Office workers' pushback against the open office environment is likely to accelerate, as illness is more easily transmitted in an open environment. Many employers already had recognized that in a competition to attract and retain top talent, squeezing workers into increasingly tight spaces was not a sustainable strategy. Now, an emphasis on social distancing and good health practices - continuing in some fashion even after the crisis has passed - may help reverse the densification trend, with less shared space and fewer workers per leased square foot.

Multifamily: Similarly, the multifamily sector could see significant upheavals as unemployment rises. Business that are closed employ people who now will struggle to pay rent. It's a similar situation to retail, only in this case the tenant is an individual or family who lost its source of income. Tellingly, Freddie Mac announced a nationwide relief plan for current multifamily borrowers and residents.

Industrial: Industrial, meanwhile, is in a two-pronged situation similar to the retail sector. Grocery and medical items, for instance, are flying off the shelves, so properties in this supply chain are humming along. But other industrial sectors could be in store for tough times, depending on what areas of the national economy slow or stop.

When the dust settles, business re-open and millions of Americans return to work it’s hard to tell what the state of the market will be. As for now, it seems everyone is doing their best to deal with the hand we’ve been dealt.

Source:

ccim.com [Article] https://www.ccim.com/cre-tenant-landlord-guidance/

Leveraging Research Coverage of the Global Health Crisis

Break Down of the Funding Programs Within the CARES Act

The paycheck protection program is a loan that was designed as a result of the Coronavirus pandemic to directly assist small business to keep their workers on payroll. But, as more time passes with the economy at a standstill more and more businesses are looking for relief. With the growing need, according to sba.gov, they are currently unable to accept new applications based on the current available appropriations funding.

The good news is that in addition to the SBA funding programs, the CARES Act established many temporary new programs to help with Coronavirus pandemic. Here is a breakdown of the current programs according to The Certified Commercial Investment Website.

IRS and Treasury Department

Deadline Extended for 1031 Exchanges: The IRS has issued guidance that indicates that the 45-day and 180-day deadlines for 1031 like-kind exchanges that would have expired from April 1 to July 14 will now expire on July 15. Watch for further details soon.

Deadline Extended for Opportunity Fund Investments: Specifically, if an investor who sold a capital asset planned to roll over the gain into an Opportunity Fund and the 180-day deadline falls between April 1 and July 15, 2020, they can make the investment on July 15 regardless of the 180-day deadline. Watch for further details soon.

Deadline to File and Pay Taxes Extended: A three-month extension has been made for tax filing and payments. Individuals will be able to defer up to $1 million without interest or penalties, and corporations can defer up to $10 million.

FEMA

FEMA Flood Insurance Renewal Extension: FEMA is extending the grace period to renew flood insurance policies from 30 to 120 days. If a policy has an expiration date between February 13, 2020 and June 15, 2020, then the NFIP insurer must receive the appropriate renewal premium within 120 days of the expiration date to avoid a lapse in coverage. Likewise, if a policyholder receives an underpayment notice dated between February 13, 2020, and June 15, 2020, then the NFIP insurer must receive the additional premium amount requested within 120 days of the date of the notice.

Federal Reserve

Federal Reserve Main Street Lending Program: The Federal Reserve Board is establishing a Main Street Lending Program to enhance support for small and mid-sized businesses that were in good financial standing before the crisis by offering 4-year loans to companies employing up to 10,000 workers or with revenues of less than $2.5 billion. Principal and interest payments will be deferred for one year. Eligible banks may originate new Main Street loans or use them to increase the size of existing loans to businesses.

Commercial Paper Funding Facility: The Federal Reserve Board will establish a Commercial Paper Funding Facility (CPFF) to support the flow of credit to households and businesses.

Facility to Facilitate Loans for Paycheck Protection Program: The Federal Reserve Board will establish a facility to facilitate lending to small businesses via the SBA's Paycheck Protection Program (PPP) by providing term financing backed by PPP loans.

The thing to keep in mind is that you need to do your research. The economy, funding and government regulations are practically changing daily. Depending on the size of your business and your needs there are a variety of different programs to assist during this time. Check the links below for further details and see which can best help you.

Sources:

ccim.com [Article] https://www.ccim.com/covid19/

sba.gov [Article] https://www.sba.gov/funding-programs/loans/coronavirus-relief-options/economic-injury-disaster-loan-emergency-advance

Are We Heading Down this Road Again???

It’s no secret that before COVID-19 was a household name, the economy was white hot. The un-employment rate was at an all time low, people were buying houses, going on vacations and investing. In a matter of months that has all come to a screeching stop. The United States economy is now filled with uncertainty, investors and businesses are watching to see when things will ‘return to normal’.

In the last 40 years the United States has seen 3 major recessions and a few smaller ones. The current economic conditions and unease brought on by the Coronavirus could very well land us in our 4th.

So, what can we do about it?

One option for commercial real estate owners and developers is a loan workout. A loan workout is when a lender is working with a borrower to get monetary or technical issue resolved. In order to successfully set up a workout with you lender here are a few basic steps to follow:

Approach your lender before any major complications arise with a detailed plan of what changes you need to make and how you plan to follow them. It’s a good idea to back this up with financial statements showing that you are able to deliver on this new promise.

Consider all aspects of the loan when you negotiate. A private lender can be much more flexible than a bank due to regulations they must follow but a few things to consider are length of term, payment schedule, interest rates and technical loan covenants.

Get it in writing! Make sure any detail that is changed, no matter how small is changed in the contract and reviewed by an attorney before the borrow signs. This will protect both the lender and the borrower to make sure the new terms are fully understood and legally sound.

If this is something you would like to look into or get more information on regarding your commercial real estate than it is a good idea to reach out to an experienced broker to help guide you through this process. John J. Godwin from Marcus & Millichap has been in the commercial real estate business for over 30 years and has fought through the ups and downs of the economy. He has worked through 3 separate economic downturns including the RTC (Resolution Trust Corporation) Disbandment, the dot-com bubble and the most recent being the Great Recession. John has worked with both lenders and borrowers during these times to create workouts that help all parties at the table continue to move forward and maneuver these uncertain times.

John’s expertise combined with the resources and connections from Marcus & Millichap, the largest national commercial real estate brokerage, gives you the strongest possible starting point. Marcus & Millichap specializes in real estate investment services with more than 2000 investment sales and financing professionals in over 80 offices thorough the United States and Canada.

If you are looking for a broker opinion of value please reach out and let John him use his expertise to help you out.

Source:

ccim.com [Article] https://www.ccim.com/cire-magazine/articles/making-it-work/?gmSsoPc=1

distressedpro.com [Article] https://www.distressedpro.com/how-to-workout-distressed-commercial-real-estate-loans/

Fiscal Stimulus Package Critical as Real Estate Investors Brace for Impact

TO WATCH FULL VIDEO, CLICK HERE.

Opportunity Zones and What you Need to Know About Them

Per the IRS.gov, “ Qualified Opportunity Zones were created by the 2017 Tax Cuts and Jobs Act. These zones are designed to spur economic development and job creation in distressed communities throughout the country and U.S. possessions by providing tax benefits to investors who invest eligible capital into these communities. Taxpayers may defer tax on eligible capital gains by making an appropriate investment in a Qualified Opportunity Fund and meeting other requirements.”

Since the inception of opportunity zones in 2017, the government has designed such zones in all 50 states, the District of Columbia and 5 U.S. Territories. In order to qualify as an Opportunity Zone the tract must be designated as a low-income community by meeting one of the following criteria. It must have a poverty rate of at least 20%, have a median family income that does not exceed 80% of the area median income, the tract must be contiguous with a designated low-income community and the median family income does not exceed 125% of the median family income in the contiguous designated low-income area.

So, how do Opportunity Zones help encourage economic development? According to the IRS, there are two ways in which they help to jump start the economy.

First, investors can defer tax on any prior gains invested in a Qualified Opportunity Fund (QOF) until the earlier of the date on which the investment in a QOF is sold or exchanged, or December 31, 2026. If the QOF investment is held for longer than 5 years, there is a 10% exclusion of the deferred gain. If held for more than 7 years, the 10% becomes 15%.

Second, if the investor holds the investment in the Opportunity Fund for at least ten years, the investor is eligible for an increase in basis of the QOF investment equal to its fair market value on the date that the QOF investment is sold or exchanged.

Now that we know what they are and where they came from, let’s talk about the incentives from an investors perspective. There are three federal tax incentives you can take advantage of as an investor to help encourage economic stimulation in these depressed areas.

Gains reinvested directly in an opportunity zone, or through an investment vehicle known as a qualified opportunity fund, are deferred until the earlier of either the sale of the investment or Dec. 31, 2026.

The basis of any investment in a qualified opportunity fund held for at least five years is increased by an amount equal to 10 percent of the amount of gain deferred under the opportunity zone program. If the investment is held for at least seven years, there is an additional 5 percent basis increase.

If a qualifying investment is held for at least 10 years, any built-in appreciation during the life of the qualifying investment is excluded from income.

The goal of opportunity zones is to produce a healthy return for the investors who are taking the risk with their capital to invest in areas that otherwise would not be considered. The benefits of this type of investment is fairly straightforward, but in a situation like this you have to consider that the risks may be just as great.

One thing to consider is that Opportunity Zones have only been around a short time and the government and IRS are still working out the kinks which means adding new rules and regulations as new issues come to light. This could put the investors at risk for unexpected tax liabilities as rules change and laws are updated. Security, compliance and transparency are huge components to successful transactions and it’s a good idea to go into this process with an independent, third party administrator to help you achieve these.

Security

The use of an independent third party to control and track the record keeping is something you will want to strongly consider. Investors will be more apt to move forward if they can trust that the data is security and being properly kept in order to provide accurate tax reporting.

Compliance

This is something you will want to pay very close attention to and track changes to prevent any unexpected tax bills as much as possible. As stated earlier, this is a newer program so you should expect the rules and regulations to change. The more you are on top of this the more prepared you will be.

Transparency

It is crucial that your administrator be transparent from day one. The complexity of this program and depending on the number of steak holders you have, this may be more difficult, but vital to keep everything running smooth and everyone happy.

Overall, Opportunity Zones can be a great investment. They can help your community and make you a great return on your investment. The key thing to remember is to do it right and keep a paper trail to help you navigate whatever changes may arise as this program continues to develop.

Sources:

irs.gov

ccim.com, article: Learning from Experience, Investing in Distressed Communities Brings Tax Benefit with New Opportunity Zone Program

marcusmillichap.com

What is the new Payroll Protection Program and How Can it Help You?

According to treasury.gov, “The Paycheck Protection Program (“PPP”) authorizes up to $349 billion in forgivable loans to small businesses to pay their employees during the COVID-19 crisis. All loan terms will be the same for everyone.” This is a loan that was designed to help small businesses keep their employees on payroll during this pandemic. More specifically, the program is for small business with less then 500 employees (including sole proprietorships, independent contractors and self-employed persons), private non-profit organizations or 501(C)(19) veterans organizations affected by coronavirus. There are some exceptions to the 500 employee limit, for further information you will need to read the SBA’s size standards for those individual industries.

The sole purpose of these loans is to cover payroll costs, most mortgage interest, rent and utility costs over the eight week period that the loan is made. Head count and compensation needs to to be maintained during this period. If these guidelines are followed the loan amount will be forgiven.

The sba.gov website states that “The loan will be fully forgiven if the funds are used for payroll costs, interest on mortgages, rent, and utilities (due to likely high subscription, at least 75% of the forgiven amount must have been used for payroll). Loan payments will also be deferred for six months. No collateral or personal guarantees are required. Neither the government nor lenders will charge small businesses any fees.”

The loan forgiveness is based upon the employer maintaining it’s head count or quickly re-hiring employees that had been let go to maintain the current salary level. If the number of employees drops or salaries decline then the amount of the loan forgiven will be reduced accordingly. The terms of the loan is 2 years at an interest rate of .5%.

“Starting April 3, 2020, small businesses and sole proprietorships can apply for and receive loans to cover their payroll and other certain expenses through existing SBA lenders. Starting April 10, 2020, independent contractors and self-employed individuals can apply for and receive loans to cover their payroll and other certain expenses through existing SBA lenders. Other regulated lenders will be available to make these loans as soon as they are approved and enrolled in the program,” according to treasury.gov.

In order to apply for a loan you can visit www.sba.gov to find a participating lender. This program will continue through June 30, 2020, but bear in mind that there is a cap on the total amount authorized by the government, so if this is something you are considering, timing is crucial as this program is evolving and changing daily.

For further details and application forms please visit the links below.

Sources:

sba.gov [Article] https://www.sba.gov/funding-programs/loans/paycheck-protection-program-ppp

home.treasury.gov [Article] https://home.treasury.gov/system/files/136/PPP%20Borrower%20Information%20Fact%20Sheet.pdf

Cost Segregation: How to Maximize Depreciation Deductions

Cost Segregation is a tool that can be used to help maximize tax benefits and should be taken into account for all commercial business owners.

When buying a piece of commercial property, new or old, the standard tax life of that property is 39 or 27.5 years. Cost segregation allows you to divide up individual components of that building and assign the correct tax life to each item giving you a larger tax break sooner than you would have if you had grouped everything together in the 39 or 27.5 year period. To give you an example, an acquired office building's price not only includes its structure (39-year tax life), but also landscaping (15-year tax life), carpeting (five- or seven-year tax life), data cabling (five-year tax life), and a number of other shorter-lived assets. In many instances, property owners unknowingly classify a property's entire depreciable basis (the purchase price minus land and other non-depreciable items) as real property. This seemingly small oversight significantly reduces the property's after-tax returns.

There have been some recent changes that make cost segregation even more valuable than it was before. Those changes take place under Bonus Depreciation. According to John Blake at ccim.com, “Bonus Depreciation allows individuals and business to immediately deduct a certain percentage of their asset costs in the first year they are placed in service. The tax law made used property eligible for bonus treatment for the first time and increased the bonus percentage to 100 percent through the tax year 2022.”

Not only is cost segregation a useful tool when purchasing a property, it can also be used during renovations. Building improvements such as plumbing, ventilation systems, and alarm system are treated as 15-year assets to give a few examples. There are other improvements that may qualify for a three, five or seven year period and qualify for bonus depreciation. A cost segregation study is crucial to make sure you are getting the best bang for your buck!

Sources:

Eric Johnston, Improving Economics [article]. https://www.ccim.com/cire-magazine/articles/improving-economics/

John Blake, CPA, The Value of Cost Segregation Studies [article].https://www.ccim.com/cire-magazine/articles/2020/winter/the-value-of-cost-segregation-studies/

Fed takes action to stem Coronavirus risk

To Watch the Full Video Click Here

Manage Transactions to Maximize Tax Benefits

Marcus & Millichap, the largest real estate firm focused exclusively on investment brokerage, is one of the industry’s leaders in 1031 exchanges. Our long-term relationships with owners and investors of every major property type allow us to match properties and exchange buyers with speed and efficiency.

So what exactly is a 1031 exchange? According to the Internal Revenue Code Section 1031 tax-deferred exchanges may look similar to simple property acquisitions in which the buyer uses funds from a previous building sale. However, these transactions entail specific closing details that differ from traditional real estate sales. Relinquished property sellers must handle earnest money and certain closing expenses properly to maximize exchange transactions' tax benefits.

Refunding Earnest Money

During most real estate sales, prospective buyers offer sellers earnest money as a down payment toward the final transaction. During 1031 exchanges many sellers want to know if they can hold the earnest money. The answer is absolutely. The Internal Revenue Service does not prohibit taxpayers from holding earnest money when executing exchange transactions, yet certain rules apply.

Once the closing takes place, the earnest money deposit becomes proceeds. If the relinquished property seller possesses the earnest money after closing, the IRS considers the deposit taxable proceeds. To avoid this, the seller should refund the earnest money to the closing. The seller incurs no gain as long as he refunds the deposit amount.

Usually problems don't arise if a real estate company or title/escrow company holds the earnest money. In that situation, the company forwards the earnest money to the closing or retains it to real estate commission, which is an allowable exchange expense.

Closing Statement Issues

In real estate transactions, the parties use closing statements, or escrow agreements, to memorialize purchase-and-sales agreement terms. The closing statement's focus is the price, but the contract can stipulate other items - such as prorated rents and property taxes, escrow account buyouts, security deposit transfers, or prepaid service contract reimbursements - that the settlement statement commonly reflects. Typically the settlement statement also shows closing costs such as attorneys' fees, real estate commissions, or transfer taxes associated with the sale. Items shown as a cost to the seller become a debit on the settlement statement and reduce the amount of proceeds available after the sale.

In exchanges, settlement statement costs to the seller reduce exchange proceeds. In addition, the IRS treats non-allowable exchange expenses charged to the seller as taxable items. Some of the more common non-allowable exchange items include prorated rents, security deposit transfers, and loan fees.

For example, a relinquished property is a rental building with an existing tenant, and the contract stipulates that the seller transfer the security deposit to the new owner.

In this situation, the IRS does not consider the security deposit a closing cost; it simply is an additional business item that happens to be associated with the sales contract. However, if the settlement statement charges the security deposit amount against the seller, the debit reduces the exchange proceeds amount. The seller probably delineates this reduction on his 8824 exchange reporting form, which requires him to pay taxes on the amount. As this example demonstrates, sellers should strive to minimize non-allowable exchange expenses during 1031 exchange closings.

Resolving Closing Statement Questions

To fix non-allowable exchange items simply, the seller should show them as paid outside closing, or POC, on the settlement statement and give the buyer a separate check. By following this procedure, these non-allowable items don't reduce proceeds and don't trigger taxable gain.

For example, Jerry is selling a $750,000 single-tenant-leased building. The closing is taking place mid-month, and the contract calls for security deposit transfer and rent proration. Jerry holds a $15,000 security deposit and $10,000 in prorated rent for the balance of the month, as well as a $7,500 earnest money deposit.

Jerry seeks advice from a 1031 professional service provider on how to minimize his tax consequences during the transaction. The tax adviser instructs the closing attorney to list the security deposit transfer and prorated rents as POC. At the closing, Jerry writes a check made payable to the buyer for $25,000 (the security deposit and prorated rent) and a check made payable to the closing attorney for $7,500 (the earnest money refund). By handling the designated non-allowable closing items and the earnest money in this fashion, Jerry ensures that his exchange transaction triggers no tax.

The appropriate handlings of earnest money and closing statements are only two of the potential complications during 1031 tax-deferred exchanges. Individuals not familiar with 1031 exchange complexities should seek qualified advice from a tax professional to achieve the desired economic benefits. Otherwise, supposed tax-free exchange transactions may leave sellers with surprise tax bills.

Sources:

Ronald L. Riatz, CCIM. 1031 Details [Article]. https://www.ccim.com/cire-magazine/articles/1031-details/

Marcus & Millichap. 1031 Exchange [Article]. https://mmreis.sharepoint.com/Departments/Marketing/Marketing/Sales%20Aids/1031%20EXCHANGE%20SALES%20AID.pdf

Three Investor Considerations to Navigate Rising Uncertainty

Raising Funds Through Sale-Leaseback Transactions

In a sale-leaseback transaction, an owner/user elects to monetize its corporate real estate facility and structure a new, long-term lease on the property to an outside investor. In exchange, the company, through the sale of the facility, receives capital to grow and revitalize it's business. The transaction has many benefits to the company, now tenant, as detailed below.

Converts Equity into Cash

With a sale-leaseback, the seller regains use of the capital that otherwise would be tied up in property ownership; at the same time, the seller retains possession and continued use of the property for the lease term.

The seller usually receives more cash with a sale-leaseback than through conventional mortgage financing. For example, if the transaction includes both land and improvements, the seller receives 100 percent of the property's market value (minus any capital gains tax). In comparison, conventional mortgage financing normally funds no more than 70 percent to 80 percent of a property's value.

Because capital gains tax reduces the cash from the sale, a sale-leaseback where the property is sold at a small gain or at a loss generally is most advantageous.

Alternative to Conventional Financing

The seller usually can structure the initial lease term for a period that meets its needs without the burden of balloon payments, call provisions, refinancing, or the other issues of conventional financing. Moreover, the seller avoids the substantial costs of conventional financing such as points, appraisal fees, and some legal fees.

A sale-leaseback also usually provides the seller with renewal options, while conventional mortgage financing has no guarantee for refinancing.

Possibility of Better Financing

Under a sale-leaseback arrangement, a buyer may be able to obtain better mortgage financing terms than the property owner. Even if the property owner defaults, the buyer is likely to continue payments to protect its equity. Thus, the lender might be willing to charge the buyer a lower interest rate, which could result in lower lease payments to the seller.

Improves Balance Sheet and Credit Standing

In a sale-leaseback, the seller replaces a fixed asset (the real estate) with a current asset (the cash proceeds from the sale).

If the lease is classified as an operating lease, the seller's rent obligation usually is disclosed in a footnote to the balance sheet rather than as a liability. This results in an increase in the seller's current ratio, or the ratio of current assets to current liabilities - which often serves as an indicator of a borrower's ability to service its short-term debt obligations. Thus, an increased current ratio improves the seller's position for borrowing future additional funds.

However, if the lease is classified as a capital lease, the advantages of the sale-leaseback arrangement from an accounting perspective are altered considerably. Statement of Financial Accounting Standards No. 13 on accounting for leases requires that a capital lease be recorded as an asset and capitalized and requires the obligation to make future lease payments to be shown as a liability.

Avoid Debt Restrictions

Businesses restricted from incurring additional debt by prior loan or bond agreements may be able to circumvent these limits by using a sale-leaseback. Rent payments under a sale-leaseback usually are not considered indebtedness for such purposes, thus a business can meet its cash needs through the sale-leaseback without violating any previous agreements.

Deterrent to Corporate Takeovers

Undervalued real estate on a company's books often serves as a target for corporate raiders. A timely liquidation through a sale-leaseback transaction may serve as a deterrent, providing management with funding to resist the takeover. In addition, a long-term lease is not as inviting to raiders as undervalued real estate.

Avoids Usury Limitations

Because a sale-leaseback is not considered a loan, state usury laws do not apply; a buyer in a sale-leaseback can earn a higher rate of return on its investment than if it had made a conventional mortgage loan to the property owner.

Sources:

Donald J. Valachi, CCIM, CPA. Sale-Lease Back Solutions [Article]. https://www.ccim.com/cire-magazine/articles/sale-leaseback-solutions/

Marcus & Millichap. Sale-Leaseback Transactions [Article].https://mmreis.sharepoint.com/Departments/Marketing/Marketing/Sales%20Aids/SALE-LEASEBACK%20TRANSACTIONS%20SALES%20AID.pdf